Утренний обзор

Обзор рынка

Зарубежные рынки

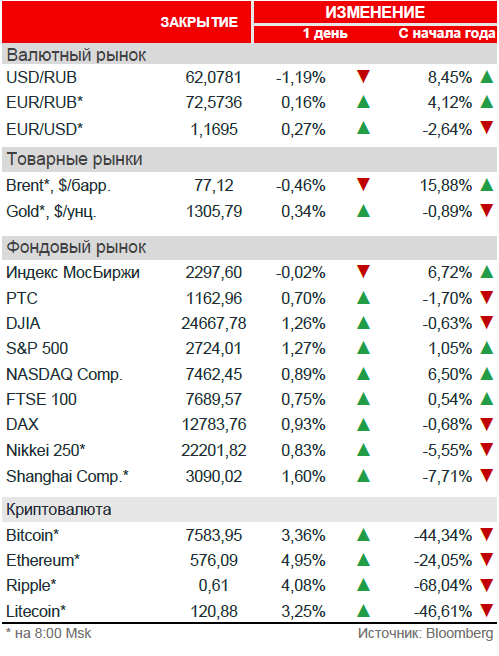

После волны продаж на фоне политического кризиса в Италии глобальные акции восстанавливались в среду. Американский S&P 500 вырос сильнее всего за три недели. Лидерами позитивного движения были акции финансовых компаний вслед за ростом доходностей десятилетних гособлигаций США. Азиатские бенчмарки также торговались в зелёной зоне.

Нефть

Котировки нефти выросли на фоне ослабления доллара. Тем не менее, внимание инвесторов остаётся направленным на возможное увеличение добычи странами ОПЕК+. Из-за выходного в США в понедельник данные по запасам нефти и нефтепродуктов будут опубликованы в четверг, консенсус-прогноз ожидает, что запасы сырой нефти за прошедшую неделю сократились на 375 тыс. баррелей.

Российский рынок

Восстановление акций на внешних площадках после падения на фоне итальянского кризиса вместе с ростом нефти оказали некоторую поддержку российскому рынку в среду. Индекс МосБиржи завершил сессию символическим снижением на -0,02%, РТС прибавил +0,70% вслед за укреплением рубля.

Бумаги Аэрофлота выросли на +6,1% до 139,85 руб. за акцию на фоне объявления о выкупе у несогласных по цене 147,22 руб. Расписки En+ на Мосбирже выросли на +6,1% на фоне сообщений об смягчении условий снятия санкций с компании. Также покупали бумаги Интер РАО (+1,7%), Мечела (ао +1,7%, ап +1,9%) и Магнита (+1,2% в Москве, +0,9% в Лондоне). Бумаги группы ТКС в Лондоне прибавили +1,2% на фоне результатов и объявленных дивидендов.

Среди аутсайдеров оказались АЛРОСА (-3,0%), X5 (-3,0%), ТрансКонтейнер (-2,5%), ТГК-1 (-2,2%) и QIWI (-1,6%).

Новости

На повестку ГОСА Аэрофлота, которое состоится 25 июня, вынесен вопрос о крупной сделке операционной аренды 50 новых воздушных судов МС-21-300. Цена выкупа акций по требованию акционеров, которые проголосуют против одобрения данной сделки или не примут участия в голосовании, определена в размере 147,22 руб. за акцию.

Bloomberg со ссылкой на источник в правительстве США сообщил, что Минфин США готов снять санкции с En+ даже в случае, если Олег Дерипаска сократит свою долю в компании всего до 40%.

X5 Retail Group объявила о структурных изменениях в торговой сети «Пятёрочка». Компания переходит на макрорегиональную модель управления. В рамках преобразований будет создано пять макрорегионов, директора которых будут подчиняться напрямую генеральному директору сети. Каждый макрорегион объединит от двух до четырёх дивизионов, сгруппированных по территориальному принципу и количеству магазинов – 2-3 тыс. универсамов. По словам компании, структурные изменения потребовались в связи с активным ростом сети – с конца 2014 «Пятёрочка» увеличила выручку и число магазинов более чем в 2 раза. Чтобы сохранить эффективность управления и не замедлять темпы развития, компания стремится освободить центральный офис от части функций. Для этого компания создаёт дополнительный, макрорегиональный уровень, который полностью возьмёт на себя операционное управление бизнесом. Таким образом, центральный офис сосредоточится на решении стратегических задач, определении целей и контроле их достижения. Это позволит повысить скорость принятия решений и качество работы с локальными промо-акциями и ассортиментом, а также лучше адаптировать магазины к региональным особенностям рынка. Сегодня уже функционирует два макрорегиона – «Москва» и «Волга». В скором времени заработает ещё три макрорегиона: «Урал-Сибирь» – с 1 июня, «Северо-Запад» – с 1 июля, «Центр-Юг» – с 1 августа. Руководить этими структурными подразделениями будут бывшие топ-менеджеры «Пятёрочки» и X5. Процесс реорганизации завершится к 1 октября 2018.

Группа ТКС опубликовала результаты за 1К18. Чистая маржа выросла на 44% г/г и составила 14,0 млрд руб. Прибыль до налогообложения увеличилась на 68% до 7,4 млрд руб. Чистая прибыль выросла на 70% г/г и составила 5,7 млрд руб. Рентабельность капитала увеличилась на 25,7 п.п. до 68,5%. Чистая процентная маржа составила 25,5% (-1 п.п. г/г). Стоимость риска снизилась на 10 б.п. до 7,5%. Совет директоров компании одобрил вторую в 2018 выплату промежуточных дивидендов за 1К18 в размере 0,24 долл. на ГДР. Доходность может составить 1,2%. Реестр закроется 14 июня.

Сбербанк объявил результаты по МСФО за 1К18. Чистая прибыль выросла на 27,3% г/г (+23,0% к/к) и составила 212,1 млрд руб. Прибыль на обыкновенную акцию составила 9,84 руб. (+26,3% г/г). Рентабельность капитала в годовом выражении достигла 24,2%, по сравнению с 23,1% годом ранее. Рентабельность активов достигла 3,1% по сравнению с 2,7% в 1К17. Чистые комиссионные доходы увеличились на 21,4% г/г до 101,5 млрд руб. в основном за счёт операций с банковскими картами. Квартальный показатель стоимости риска составил 105 б.п., что на 44 б.п. ниже к/к. Отношение операционных расходов к операционным доходам улучшилось до 33,6% по сравнению с 34,7% годом ранее. Кредиты до вычета резерва под обесценение (включая кредиты, оцениваемые по амортизированной стоимости, и кредиты, оцениваемые по справедливой стоимости) увеличились на 1,1% до 20,1 трлн руб. Розничный кредитный портфель вырос на 3,5% до 6,0 трлн руб., преимущественно за счёт роста ипотечного портфеля на 4,8% и потребительских кредитов на 3,6% за квартал. Коэффициент достаточности базового капитала 1-го уровня по стандарту Базель III составил 12,2%, что на 100 б.п. выше по сравнению с началом года.

Газпром представил отчётность по МСФО за 1К18. Выручка от продаж (за вычетом акциза, НДС и таможенных пошлин) увеличилась на 18% г/г и составила 2,138 трлн руб. Увеличение выручки от продаж в основном вызвано ростом продаж газа и продуктов нефтегазопереработки. Величина прибыли, относящейся к акционерам ПАО «Газпром», составила 371,623 млрд руб., что на 11% больше г/г. Чистый долг увеличился на 1% до 2,410 трлн руб. по состоянию на 31 марта 2018. Рост связан с увеличением суммы долгосрочных кредитов и займов, что было частично компенсировано увеличением остатков денежных средств и их эквивалентов.

Аэрофлот сообщил результаты 1К18 по МСФО. Выручка увеличилась на 8,5% г/г до 111,942 млрд руб. Показатель EBITDAR снизился на 21,6% г/г и составил 10,767 млрд руб. Чистый убыток увеличился в 2,2 раза и достиг 11,543 млрд руб. Общий долг по состоянию на 31 марта 2018 снизился на 11,5% с начала года и составил 92,718 млрд руб. Снижение долговой нагрузки связано с переоценкой обязательств по финансовой аренде вследствие укрепления рубля к доллару. По состоянию на 31 марта 2018 объём невыбранных лимитов по кредитным линиям, доступным группе, составлял 99,1 млрд руб.

Полюс опубликовал финансовый отчёт по МСФО за 1К18. Объём реализации золота составил 459 тыс. унций, сократившись на 23% к/к, или на 6% г/г. Выручка составила 617 млн долл., снизившись на 17% к/к и увеличившись на 1% г/г. Снижение в квартальном сопоставлении вызвано сокращением объёма реализации (включая флотоконцентрат) на фоне снижения производства золота (аффинированное золото и золото в концентрате) на 13% к/к в связи с увеличением запасов на аффинажном заводе и промплощадке. Скорректированный показатель EBITDA снизился на 17% к/к и вырос на 1% г/г, составив 387 млн долл. Причиной сокращения по сравнению с предыдущим кварталом явилось снижение объёма реализации. Рентабельность по скорректированному показателю EBITDA не изменилась, составив 63%. Прибыль за период сократилась до 244 млн долл., снизившись на 9% к/к и на 51% г/г, что частично обусловлено снижением операционной прибыли и эффектом неденежных статей, таких как прибыль от инвестиций и переоценка стоимости производных финансовых инструментов, а также прибыль от курсовых разниц. Скорректированная чистая прибыль снизилась на 8% к/к и увеличилась на 10% г/г, составив 223 млн долл.

ФосАгро отчиталась о результатах за 1К18 по МСФО. Выручка выросла на 23% г/г до 54,6 млрд рублей (960 млн долларов). EBITDA достигла 14,3 млрд рублей (251 млн долларов), увеличившись на 13% г/г, рентабельность по EBITDA составила 26% (-3 п.п. г/г). Чистая прибыль сократилась на 44% г/г до 6,8 млрд руб. Чистая прибыль, скорректированная на неденежные валютные статьи, выросла на 13% г/г до 6,3 млрд рублей (111 млн долларов).

Акрон объявил результаты по МСФО за 1К18. Выручка составила 24,050 млрд руб., изменившись незначительно г/г. В долларовом эквиваленте выручка выросла на 3% до 423 млн долл. Показатель EBITDA вырос на 7% г/г до 7,958 млрд руб. В долларовом эквиваленте показатель EBITDA вырос на 11% до 140 млн долл. Уровень рентабельности по EBITDA составил 33% против 31% годом ранее. Чистая прибыль выросла в 2,6 раза г/г до 4,146 млрд руб. (73 млн долл. США). Чистый долг вырос на 4% с начала года и составил 62,738 млрд руб. В долларовом эквиваленте данный показатель вырос на 5% до 1,096 млрд долл. Отношение чистого долга к EBITDA составило 2,1 против 2,0 на конец 2017 года. В долларовом эквиваленте данный показатель также составил 2,1 против 2,0 на конец 2017 года.

МКБ объявил результаты деятельности за 1К18 по МСФО. Чистая прибыль составила 2,3 млрд руб. (-50,1% г/г). Чистые процентные доходы увеличились на 24,8% г/г до 13,0 млрд руб. Чистая процентная маржа составила 3,0% (без изменений г/г). Чистая процентная маржа по взвешенным с учётом риска активам увеличилась до 5,0% по сравнению с 4,3% годом ранее. Показатели рентабельности собственного капитала и рентабельности активов сократились до 6,9% и 0,5%, соответственно, что обусловлено влиянием отрицательной валютной переоценки на чистую прибыль. Активы сократились на 1,5% и составили 1,9 трлн руб. Совокупный кредитный портфель до вычета резервов сократился на 15,3% с начала года и составил 693,9 млрд руб., что связано с рядом крупных погашений в 1К18. Доля NPL (кредитов, просроченных свыше 90 дней) в совокупном кредитном портфеле сохранилась на уровне начала года и составила 2,4%. Стоимость риска (COR) снизилась с 2,5% на начало года до 0,6% за 1К18.

Рыночные индикаторы

Календарь корпоративных событий

| 31.05 | Газпром | результаты МСФО 1К18 |

| Акрон | ГОСА | |

| САФМАР ФИ | результаты МСФО 1К18 | |

| Транснефть | совет директоров (дивиденды 2017) | |

| 01.06 | Транснефть | результаты МСФО 1К18 |

Календарь ключевых макроэкономических событий

| Чт | 31 мая |

✔ Япония: промышленное производство |

| Пт | 1 июня |

✔ Россия: вступление в силу результатов ребалансировки индексов MSCI, |