Утренний обзор

Обзор рынка

Зарубежные рынки

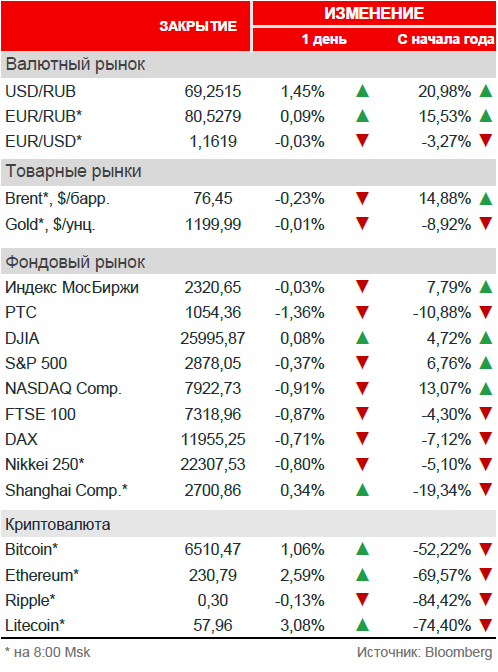

Американские индексы в четверг выросли, в очередной раз отыгрывая комментарии Д. Трампа. Президент США заявил, что рассматривает возможность возвращения в Трансатлантическое партнёрство. Кроме того, президент снял напряжённость вокруг торгового противостояния США и Китая, заявив, что две страны могут и не ввести новые пошлины друг против друга. Динамика на азиатских площадках была смешанной.

Нефть

Нефть, ранее подскочившая на фоне усиления напряжённости на Ближнем Востоке, в среду стабилизировалась. Стоит отметить, что геополитические новости были в центре внимания участников рынка, в то время как инвесторы не обратили особого внимания на данные о неожиданном росте запасов сырой нефти в США.

Российский рынок

Российский рынок в четверг продолжил постепенное восстановление, чему поспособствовал позитивный внешний фон, а также смягчение риторики американской стороны после громких событий и заявлений последних дней. Президент США Дональд Трамп, пригрозивший накануне ракетным ударом по Сирии, заявил, что не говорил о конкретном времени атаки. Глава Минфина США Стивен Мнучин заявил, что Вашингтону не следует вводить санкции против госдолга РФ, несмотря на то что Конгресс США предложил соответствующий законопроект. Подобный фон позволил рублю перейти к восстановлению, подняв вслед за собой и долларовый индекс РТС. Индекс МосБиржи завершил четверг ростом на +0,82%, РТС прибавил +3,84%.

В лидерах роста были ДВМП (+11,0%), Мечел (ао +7,2%, ап +3,6%), Лента (+6,1%), Норильский никель (+4,9%) и Русал (+4,1%).

Аутсайдерами стали Яндекс (-3,5%), Мегафон (-2,3%), ЛУКОЙЛ (-2,2%), Полиметалл (-2,1%) и НЛМК (-1,9%).

Новости

Детский мир опубликовал операционные результаты за 1К18. Выручка выросла на 14,0% г/г до 24 млрд руб., при этом выручка интернет-магазина росла опережающими темпами +64,9% г/г и достигла 1,5 млрд руб. Сопоставимые продажи (like-for-like) выросли на 5,1% г/г за счёт увеличения числа чеков на 8,8% при снижении среднего размера чека на 3,4%. Компания открыла 5 новых магазинов, общая торговая площадь увеличилась на 15,1% г/г до 686 тыс. кв. м.

Олег Дерипаска отозвал свою кандидатуру в совет директоров Норильского никеля.

СМИ со ссылкой на источники сообщают, что правление ГАЗПРОМа рекомендует дивиденды за 2017 год в размере 8,04 руб. на акцию – на уровне прошлого года. В новости нет ничего неожиданного: компания ранее уже заявляла, что планирует сохранить дивиденды на уровне 2016.

Газпром нефть 20 апреля обсудит дивиденды за 2017.

Transportation Investments Holding Ltd. завершила продажу 30,75% доли в Global Ports группе Дело. О сделке было объявлено 20 декабря 2017. Сумма сделки не раскрывается.

Русская Аквакультура объявила результаты за 2017 по МСФО. В 2017 группа продолжила начатый в конце августа 2016 вылов и реализацию товарной продукции, что позволило удвоить выручку до 5,0 млрд руб. по итогам 2017. Скорректированный показатель EBITDA увеличился на 36,4% до 2,1 млрд руб. Маржа по показателю скорректированной EBITDA составила 41%. Большую часть полученной выручки компания продолжила направлять на снижение долговой нагрузки, и по состоянию на 31 декабря 2017 чистый долг составил 742,4 млн руб. по сравнению с 3 166,1 млн руб. по состоянию на 31 декабря 2016 (-76,6% г/г). Соотношение чистого долга к скорректированному показателю EBITDA на конец 2017 составило 0,36х по сравнению с 2,09х на 31 декабря 2016. По общепринятому в аквакультурной отрасли показателю оценки эффективности производственной деятельности, операционный EBIT/кг реализованной продукции, компания по итогам 2017 показала результат на уровне мировых лидеров отрасли – 178,5 руб./кг, улучшив результат относительно 2016 на 8,2%. На показателе чистой прибыли от продолжающейся деятельности сказалось отсутствие зарыбления в 2016 и соответствующей переоценки биологических активов. Данный разовый фактор, оказывающий влияние на показатели компании в 2017-2018, будет нивелирован до конца 2018 благодаря завершению очередного цикла зарыбления 2017 года.

Криптовалюты

Криптовалютный рынок вчера проснулся, а сегодня побежал! Биткоин вырос на 14% (7800 долл.), в то время как альткоины набирают ещё большую силу, некоторые альткоины взлетают на 30-40%. Доминирование биткоина упало ниже 42%, обороты рынка подскочили почти в 2 раза до 25 млрд долл., капитализация рывком в 14% выросла до 315 млрд долл. Этап консолидации, похоже, закончился, и нас ждёт новое ралли. Учитывая, что падение биткоина с рекордных 19500 долл. в декабре до почти 6000 долл. в марте было самым затяжным и сильным падением за его историю, новое ралли может стать столь же впечатляющим.

Рыночные индикаторы

Календарь корпоративных событий

| 13.04 | НЛМК | операционные результаты 1К18 |

Календарь ключевых макроэкономических событий

| Пт | 13 апреля | ✔ ЕС: торговый баланс ✔ США: количество буровых установок |